The United States has rightly embraced industrial policy again but is leaving a critical part of industry behind. Washington’s major economic support schemes overwhelmingly favor large, “mega-cap” companies focused on foundational and capital-intensive technologies while neglecting “mid-cap” companies that scale production, sustain manufacturing and anchor domestic supply chains. “Mid-cap” companies form the backbone of the nation’s industrial base and workforce but sit in a persistent policy blind spot. Thankfully, if policymakers acknowledge this gap there are solutions ready to support these critical companies and industries.

“Mid-cap” companies are defined here as those with annual revenue between $1 -10 billion dollars. These companies translate technology innovation into commercialized and scaled products that anchor domestic manufacturing capability. Despite their criticality, in current industrial policy discussion, “mid-cap” companies receive comparatively little attention.

The consequences of this neglect are already visible in several areas of U.S. industrial policy. The United States spent heavily to subsidize foundational semiconductor technologies, but chips do not create strategic advantage on their own. Intense policy focus on foundational segments alone ignores the fact that semiconductors must be designed into products that consumers ultimately use. Mid-cap companies that sell those end products, particularly in deep tech and hardware sectors facing Chinese state-sponsored competition, should be protected and promoted as well.

Consider, will U.S. industrial policy be a success if frontier American AI models and semiconductors are integrated into foreign-designed, developed, manufactured, and controlled robots, power equipment, medical devices, and commercial products across the domestic economy?

This “missing middle” phenomenon, where mid-sized firms are underrepresented or under-supported relative to their potential role in innovation and productivity, has been well-documented in economic and strategy literature.1 For instance, research highlights how policy distortions such as regulatory burdens and mismatched financing can hinder mid-sized firms from scaling, leading to gaps in market representation and economic output.2 In the context of U.S.-China strategic competition, this gap is exacerbated in deep tech and hardware where U.S. ventures excel in early-stage innovation but struggle with scale-up financing for hardware-intensive technologies, allowing China to capture manufacturing leadership through aggressive state subsidies and coordination.3

China’s industrial strategy highlights that this gap is avoidable. Beijing does not sharply distinguish between upstream inputs and downstream products. Instead, it aligns financing, procurement, and regulation to shepherd the commercialization of technologies into manufactured goods. By supporting firms across the value chain, particularly when faced with the challenges of scaling production, Beijing has enabled domestic companies to move rapidly from early capability to scaled manufacturing and global competitiveness.

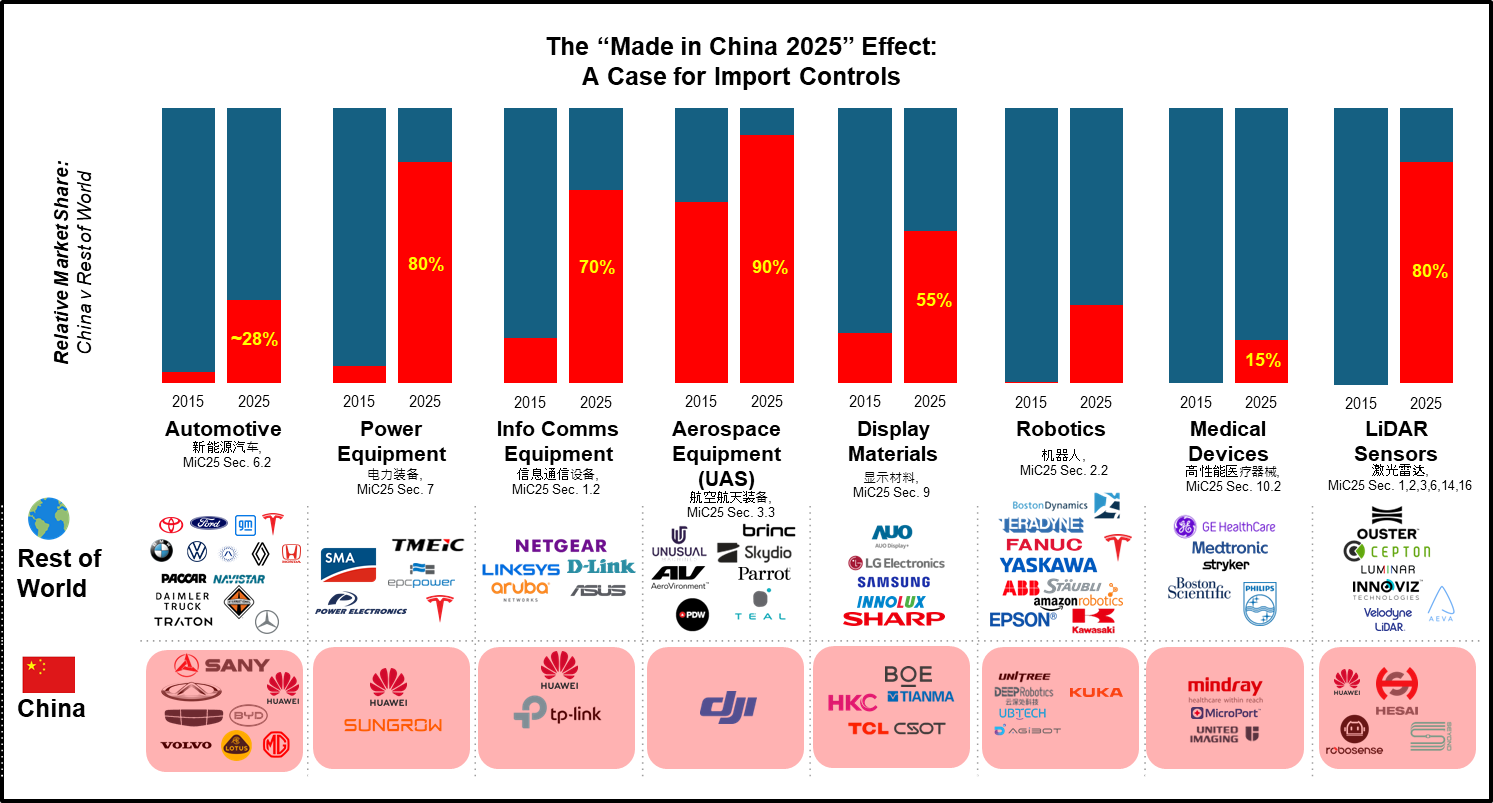

This approach is evident across multiple sectors. In semiconductors, Chinese firms such as SMIC, YMTC, CXMT, HiSilicon, and NexChip entered nearly every segment of the market through massive subsidies4, below-market loans5, and forced technology transfers6. In batteries, despite U.S. firms inventing lithium-ion technology, China now controls roughly 76 percent of global production.7 Under its Made in China 2025 strategy, Beijing has prioritized downstream industries including new energy vehicles, robotics, medical devices, and advanced manufacturing, using subsidies estimated at three to nine times those of OECD countries to accelerate scale and undercut competitors.8 See Figure 1.

Against this backdrop, the limits of U.S. industrial policy become clear. Although the United States can secure production of bleeding-edge semiconductors and even begin to domesticate or “near-shore” production of lagging-edge semiconductors, the American mid-cap technology companies competing to sell products that use those semiconductors are not receiving the same level of attention or support. This insufficient policy focus stems from structural limits in U.S. venture capital, which prioritizes short-term lifecycles mismatched to the 10-15 years needed for deep-tech and hardware commercialization and federal programs that either target early research and development or mega-cap established firms. As a result, mid-cap companies deploying cutting-edge products risk being undercut, eroding the U.S. industrial capacity necessary for mobilization in time of conflict. By failing to adequately support and incentivize mid-cap technology companies, the United States risks undercutting its own industrial policy and failing to secure the commercialization and manufacturing scale for the foundational technologies and commodities that it promotes.

The CHIPS and Science Act (“CHIPS Act”) offers a clear illustration of this phenomenon. The Act reflected a widely accepted economic logic that national security is a public good and that market failures can justify targeted government intervention. By that measure, CHIPS has succeeded. Semiconductor firms such as Qualcomm, Micron, Intel, GlobalFoundries, and TSMC are now building fabrication plants across the United States, reversing decades of manufacturing decline.

But the CHIPS Act also highlights what U.S. policy leaves untouched. It did little to support the mid-cap firms responsible for designing, manufacturing, and selling the products that incorporate those chips. Venture capital timelines remain mismatched to deep-tech and hardware commercialization, and federal programs continue to prioritize large incumbents with programs that are unlikely to yield tangible benefits for many years. The result is a growing gap between foundational capability and industrial resilience.

A similar pattern is emerging in recent critical minerals policy. Substantial public and private investments have flowed into mining and extraction, yet far less attention has been paid to the downstream firms required to process materials, manufacture components, and insulate the broader economy from coercion.

Another example is playing out in additive manufacturing. Chinese firms like Bright Laser Technologies, Eplus3D, and Farsoon have rapidly expanded their position in aerospace and industrial metal printing, deploying multi-laser systems that rival leading German and American technologies at significantly lower prices. At the same time, American mid-cap firms such as VulcanForms, Hadrian, Machina Labs, Divergent 3D, and Matter are attempting to rebuild the U.S. industrial base through automated, digitally native manufacturing. These mid-cap firms are not systematically receiving any government support, even though developing and scaling innovative and autonomous manufacturing processes are essential to America’s reindustrialization.

Further, these companies represent the industrial capacity of the future, designing products and systems for factories that can switch from making car parts to military materiel in time of need. If these American mid-cap competitors are undercut by subsidized Chinese hardware, the United States loses another market and the physical ability to rapidly manufacture defense assets in a conflict.

The U.S. government should endeavor to support its mid-cap technology companies just as it supported domestic and allied semiconductor companies. Because these markets and industries are not as capital-intensive as semiconductor manufacturing, simple regulatory relief as opposed to direct government subsidy is sufficient to level the playing field. One potential solution is generating demand for American-made products by limiting PRC firms’ access to critical domestic markets. Washington has piloted this policy tool in the automotive sector, limiting PRC firms from critical automotive supply chains and thereby generating demand for products from American mid-cap suppliers, and there are early signs of success.9

Washington has also turned to tariffs to promote domestic manufacturing, but tariffs are not a sufficient solution. Paradoxically, tariffs and trade remedies can raise input costs for manufacturers reliant on imported subcomponents. While these tools can encourage domestic production in some contexts, they can also strain precisely the firms U.S. industrial policy should seek to preserve.

For all these reasons, U.S. industrial policy must not continue to miss the middle. The United States cannot and should not attempt to replicate China’s subsidy model or control its entire economy. It does not need to. Because many downstream industries are less capital-intensive than semiconductor manufacturing, targeted and proportionate measures can provide meaningful relief.

After recognizing the gap in current federal industrial policy, policymakers should consider developing patient capital facilities coordinated across the Department of War, Department of Energy, and trusted private capital allocators, demand-side coordination of government anchor clients, targeted budget-neutral tax reform that creates incentives for scaled manufacturing, and regulations like the Department of Commerce’s connected vehicle supply chain rule that insulate American supply chains in critical sectors from untrusted products. Just as the U.S. government acted to secure semiconductor and automotive supply chains, it can and should extend similar logic to other critical industries.

With limited industrial policy intervention, the U.S. government can avoid an outcome where it succeeds in protecting foundational technologies while ceding the industries that put those technologies to work. An industrial policy that misses the middle does not just fall short; it fails on its own terms.

Jonathan Oldstyle is a federal employee with previous experience at the National Security Council, the Department of Defense, and on Wall Street.

The views expressed in this article are solely those of the author and do not represent the official views or policies of the U.S. Government or any of its agencies.

Tybout, James. “The Missing Middle, Revisited.” Correspondence in Journal of Economic Perspectives 28, no. 4 (Fall 2014): 235–36. American Economic Association.↩︎

Khan, Fatima Faisal. The Missing Middle: How to Close America’s Deep-Tech Financing Gap in Strategic Competition with China. Washington, DC: Institute for Security and Technology, October 2025. Institute for Security and Technology.↩︎

Hsieh, Chang-Tai, and Benjamin A. Olken. “The Missing ‘Missing Middle.’” Journal of Economic Perspectives 28, no. 3 (Summer 2014): 89–108. American Economic Association.↩︎

“China Sets Up Third Fund with $47.5 Bln to Boost Semiconductor Sector.” Reuters, May 27, 2024. Reuters.↩︎

Organisation for Economic Co-operation and Development. “Measuring Distortions in International Markets: Below-Market Finance.” OECD Trade Policy Papers, No. 247, December 2019. OECD↩︎

Kevin Purdy, "Stratasys Sues Bambu Lab over Patents Used Widely by Consumer 3D Printers," Ars Technica, August 12, 2024, Ars Technica.↩︎

Shanghai Metals Market. “Chinese Li-ion Battery Market: Ways to Survive under Fierce Competition.” Metal.com, April 18, 2025. Metal.com.↩︎

Kiel Institute for the World Economy. “China’s Massive Subsidies for Green Technologies.” News, April 10, 2024. Kiel Institute.↩︎

Stephen Wilmot, “The Car Industry Is Racing to Replace Chinese Code,” The Wall Street Journal, February 6, 2026, Wall Street Journal↩︎