Introduction

Over the past several years, the increasing relevance of economics in national security has galvanized policymaker attention towards both incremental and transformational concepts to reimagine U.S. economic statecraft and economic security capabilities (along with its bureaucracy). One transformational proposal gaining policymaker attention seeks to create a new “Department of Economic Security” (DES) within the executive branch to consolidate functions from across ostensibly siloed departments and agencies. Based on our experiences in government, we think that such a well-intentioned transformational effort will take significant time, bureaucratic deconfliction efforts, and unidentified fiscal outlays to achieve. Instead, policymakers should start with reforming the Treasury Department’s national security functions.

This analysis proceeds in three sections. First, it assesses the current policy proposals involving a DES. Next, it dissects a case study involving the challenges establishing a much smaller economic statecraft bureaucratic innovation involving economic analysis of sanctions through the Treasury Department’s Sanctions Economic Analysis Division (SEAD). The paper concludes with a more modest but nonetheless ambitious proposal to reorganize the Treasury Department’s Office of Terrorism and Financial Intelligence (TFI) into the Office of National Security and Financial Crimes (NSFC) to transition from its 9/11-era mandate to address emerging threats. Most importantly, these recommendations are designed to start a more deliberate and concerted dialogue among public and private stakeholders to catalyze urgent reforms around organizational design and resourcing. Importantly, this paper does not attempt to resolve ongoing definitional debates over economic security and economic statecraft; Rachel Lyngaas and colleagues address this issue in an April 2026 piece.

For the purposes of this paper, two related but distinct concepts warrant clarification. This paper uses economic security to describe the broad domain of policies aimed at protecting domestic economic resilience and strategic capacity, and economic statecraft to describe the specific deployment of economic tools to influence foreign actors—whether collaboratively, as in trade agreements, or coercively, as in sanctions. The distinction matters because the case for Treasury leading differs across the two concepts. In economic statecraft, Treasury already leads, through OFAC’s sanctions authorities and TFI’s financial-intelligence apparatus. In economic security broadly construed—supply-chain resilience, industrial policy, technology competition—Treasury is one player among many, and not the natural lead. The reform proposed here is therefore bounded: it strengthens Treasury where it already has comparative advantages rather than asserting a claim over the whole of economic security. Properly understood, this expanded mandate is not a departure from Treasury’s core statutory responsibility to protect the integrity of the U.S. and global financial systems—it is an extension of it. The same financial system Treasury safeguards is the medium through which modern economic statecraft operates; building the capacity to wield and analyze financial measures is therefore continuous with, not a distraction from, Treasury’s mission.

What is the “Department of Economic Security”?

Prominent voices support a new economic security bureaucracy. Then-Deputy National Security Advisor Daleep Singh recommended in January 2025 that the United States “consider” a cabinet-level economic security function, though without a detailed blueprint. In November 2025, Congress’s U.S.-China Economic and Security Review Commission recommended a “consolidated economic statecraft entity” merging export-control and sanctions functions across Commerce, Treasury, State, and Defense.

Not all reform voices favor a new department. Former Deputy Treasury Secretary Justin Muzinich has instead called for new dedicated offices within Treasury and Commerce, and later co-chaired the Council on Foreign Relations’ 2025 Task Force on U.S. Economic Security, which proposed a coordinating “Economic Security Center” at Commerce rather than a new department. His diagnosis is one we share: as he argued, TFI “does not have the necessary infrastructure or personnel to navigate a potential great-power economic conflict.” The CFR approach is complementary to ours—it targets economic security and sits at Commerce, while this reform targets the economic statecraft node that sits at Treasury, addressing a different half of the same fragmentation problem. Former National Security Advisor H.R. McMaster and Andrew Grotto similarly favored an executive order over institutional reform.

Others have floated coordinating bodies short of a department. The Potomac Institute’s 2025 Economic Statecraft Summit report urged a cabinet-level entity to “orchestrate” statecraft across the more than 1,400 offices that share these authorities, while a 2026 Foundation for Defense of Democracies memo proposed an “Economic Pentagon” control center that explicitly rejects a “massive new bureaucracy.”

While attractive in theory, establishing an entirely new government agency is practically unachievable in the short term. DES cannot and will not be created in a vacuum. Rather, the current political and bureaucratic environment makes a massive executive branch overhaul untenable. Even as a signature initiative of a future presidential administration, implementation of DES will take years and suffer from extensive bureaucratic growing pains. The most instructive precedent is the post-9/11 creation of the Department of Homeland Security (DHS), whose troubled consolidation illustrates the operational and political pitfalls that a comparable economic security reorganization would invite.

At an operational level, a new cabinet department would repeat the costly, years-long stand-up that the post-9/11 creation of DHS illustrates: migrating statutory authorities—OFAC’s designations, FinCEN’s Bank Secrecy Act authorities, the Commerce Department’s Bureau of Idustry and Security’s (BIS) export-control licensing—would invite protracted litigation and rulemaking, while securing facilities, systems, and staff would consume leadership attention before any mission work could scale. DHS took control of its headquarters site in 2004 but did not complete the move for fifteen years; America’s economic statecraft cannot wait that long.

Consolidation could also diminish rather than amplify these tools. Offices like OFAC and BIS draw strength from sitting inside larger departments that can marshal political capital and supporting capabilities—OFAC, for instance, relies on Treasury’s Office of Intelligence and Analysis for sanctions targeting. Stripping them into a smaller standalone department risks an entity that achieves less than the sum of its parts.

The DES concept is sometimes modeled on Japan’s 2022 creation of a cabinet minister for economic security. But that was a ministerial portfolio within the prime minister’s office—one that also spans science, technology, and space policy—not a bureaucratic consolidation; implementation remains spread across Japan’s finance, trade, and foreign ministries.

Neither the Singh nor U.S.-China Economic and Security Review Commission proposals contend with a more basic proposition: appropriately resource existing civilian institutions. As Alex Zerden and Leland Smith described in a 2024 War on the Rocks analysis, Congress and successive administrations “expect too much from its civilian economic statecraft workforce without sufficiently resourcing them.”

Funding levels reinforce the point. The two civilian agencies that actually wield these authorities—Treasury’s TFI and Commerce’s BIS—operate on a combined direct appropriation of roughly $893 million, a fraction of what a new department would cost to stand up. Even the Defense Department’s newly created Economic Defense Unit was funded at $593 million for FY2027, despite holding none of the coercive financial authorities that give economic statecraft its force.

Lessons Learned from the Sanctions Economic Analysis Division

The case for targeted reform over wholesale reorganization is grounded in our recent experiences. A 2023 attempt to create a new sanctions analytic capability within the Treasury Department demonstrates the operational and organizational challenges of building new functions, even at the smallest scale.

In October 2021, the Treasury Department’s Sanctions Review (2021 Review) diagnosed a fundamental gap: the department lacked dedicated economic analytical capacity to assess the impact of sanctions before and after implementation. The 2021 Review called for “rigorous economic analysis, technical expertise, and intelligence” to be incorporated into a structured sanctions policy framework. In April 2023, the Sanctions Economic Analysis Division (SEAD) was established within TFI to fill that gap. Two years later, the Government Accountability Office’s (GAO) September 2025 assessment of Russia sanctions found that no agency—including the Treasury Department—had established objectives linked to measurable outcomes. A senior OFAC official told GAO that SEAD lacked “an analytical construct to assess its sanctions programs systematically.” The analytical infrastructure the 2021 Review called for had not fully materialized–not because the diagnosis was wrong but because the institutional design of the solution created predictable friction.

SEAD had a clear mission: firm- and industry-specific analysis of proposed sanctions’ collateral effects, after-action analysis of OFAC actions, and mitigation recommendations. It reported jointly to OFAC—its institutional home—and the Office of International Affairs (IA). In practice, national security priorities pulled the office toward energy markets, commodities, and country-level work—valuable analysis, but a departure from its mandate, and one that put SEAD in recurring jurisdictional tension with IA, which viewed macroeconomic sanctions analysis as its own turf. The mission drift was predictable. OFAC is an enforcement agency operation—designations, compliance, investigations—with visible outputs. SEAD is an analytical function whose value lies in informing decisions others make. Embedding an analytical function inside an enforcement organization creates structural tension: the host’s rhythms, incentives, and operational tempo absorb the new function rather than accommodate it. Economists need sustained desk time; OFAC runs on meetings and deliberation. And because demand for SEAD products came primarily from outside OFAC—from Treasury principals and interagency consumers—the office’s administrative home and its analytical clients were structurally misaligned.

The office was also institutionally fragile, controlling almost none of its own critical resources—the central concern of resource dependence theory This fragility was not unique to SEAD; the GAO report documented the same pattern across agencies, where analytical teams were built on supplemental funding that expired, offices conducted critical analysis with one or two people, and no risk assessments existed for when the money ran out. Research on organizational ambidexterity points to the design lesson: new functions need structural separation—their own leadership, culture, and budget—while staying strategically integrated at senior levels.

Coordination costs compounded these problems. SEAD’s written products were typically tasked by Treasury principals, coordinated through the TFI Front Office, and cleared for wider dissemination by three separate policy offices—each with its own review process. Since SEAD’s products were always grounded in economics, a single clearance pathway through an economics-oriented office would have reduced friction without sacrificing rigor.

SEAD's experience points to a design principle that applies well beyond sanctions: analytical functions belong in organizations that match their professional culture; structural independence from enforcement is necessary for credible evaluation; and if a policy tool is permanent, its analytical infrastructure should be too. The 2021 Review devoted extensive attention to the policy framework for sanctions and considerably less to the organizational architecture through which that analysis would be delivered. None of this is to discount leadership: capable principals can mitigate poor design, just as weak ones can squander good design. But durable analytical capacity should not depend on the disposition of whoever holds the office, and the structural features described here recur across agencies regardless of leadership quality.

Reimagining the Treasury Department’s Office of Terrorism and Financial Intelligence

Rather than create a new bureaucracy from scratch, policymakers should consider more achievable and lower friction interventions in the short term to improve economic statecraft and the financial dimensions of economic security capabilities. Limited but structural reforms to TFI is one place to start.

More than twenty-one years have passed since Congress created TFI. In that time, TFI has pioneered the targeted use of financial sanctions, financial intelligence information, financial regulation, and international standard setting to support U.S. foreign policy and national security objectives “while also protecting the integrity of the U.S. and global financial systems.” Financial sanctions in particular have become a “tool of first resort,” as noted by the 2021 Review and other analyses.

Two decades of experience provides a sufficient record to consolidate successes and also identify changes to reorient the organization for current and anticipated economic statecraft challenges. Put bluntly by Muzinich, TFI “is not a team built to analyze the complex economic and financial links that would be implicated in a great-power clash.”

TFI’s analytical demands have expanded well beyond its 9/11-era design. Sanctions programs have grown more than 1,000 percent; AML/CFT policy has shifted toward risk-based frameworks that presuppose quantitative evidence that TFI has no permanent capacity to produce; and when high-stakes operational decisions have required serious macroeconomic analysis—the Russia oil price cap being the clearest example—that work has fallen to other Treasury offices whose mandates do not include national security.

The Current Architecture

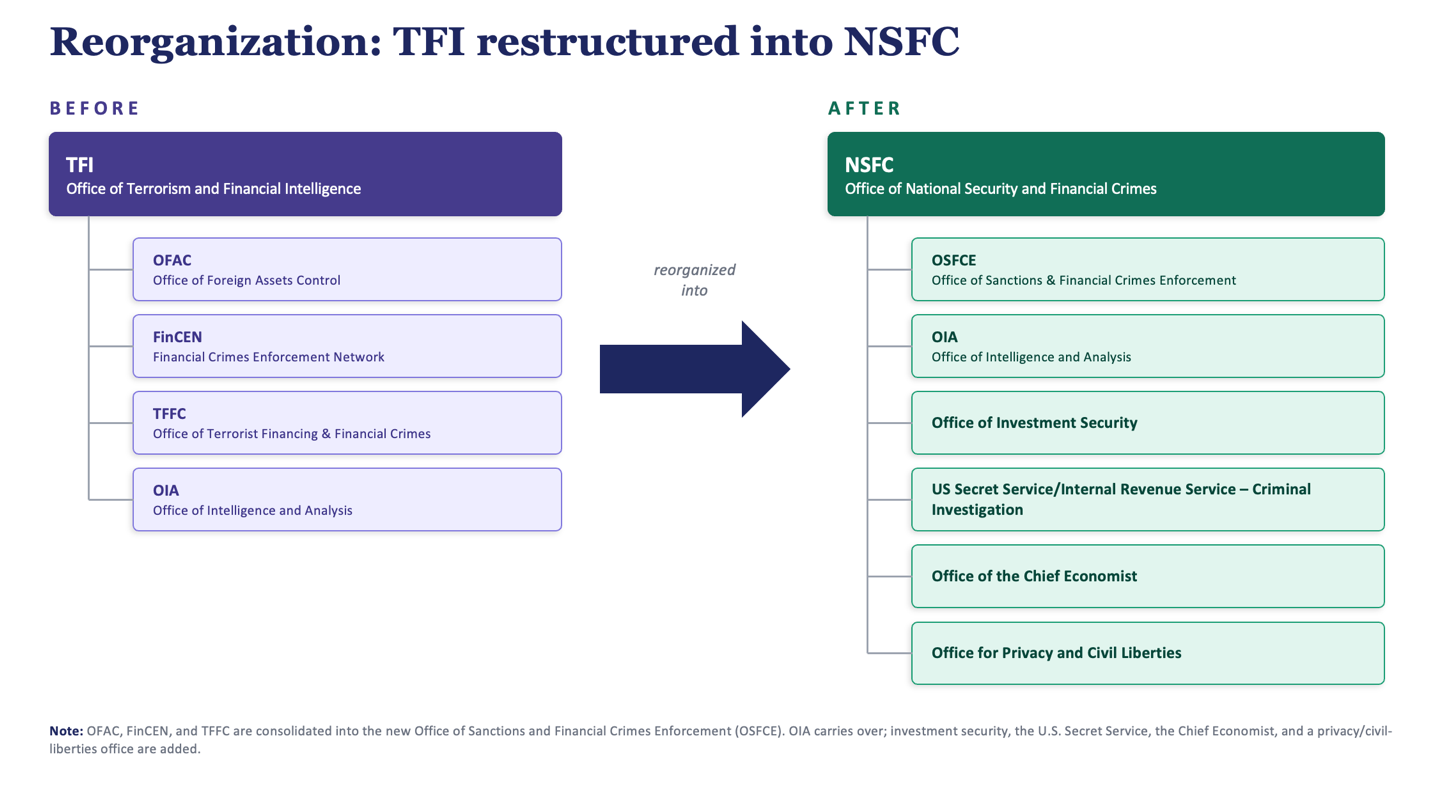

TFI currently supervises four primary component offices and bureaus with complementary, and sometimes overlapping, mandates (The Treasury Office for Asset Forfeiture is a fifth administrative component of TFI but its mandate is separate from TFI and therefore outside of the scope of this analysis.).

OFAC administers economic sanctions.

FinCEN is the U.S. financial intelligence unit and primary federal anti-money laundering and countering the financing of terrorism (AML/CFT) regulator.

The Office of Intelligence and Analysis (OIA) is an element of the Intelligence Community (IC) and supports the other components and Treasury Department leadership.

The Office of Terrorist Financing and Financial Crimes (TFFC) is the TFI policy and strategy office.

As with other bureaucracies, the overlapping mandates of the TFI components create internal bureaucratic challenges in addition to complications when engaging with intragovernmental and nongovernmental stakeholders. For instance, TFI currently has three offices with a policy mandate: TFFC (as its primary function), OFAC’s Policy Division, and FinCEN’s Policy Division. Furthermore, TFI contains two intelligence-focused elements: OIA (the IC function) and FinCEN’s Research and Analysis Division (formerly called the Intelligence Division).

For a bureaucracy with about 1,000 employees, these functions appear to duplicate rather than amplify the office’s capabilities. And to be clear, the focus for reform is not on TFI’s workforce. Rather, the recommendations address organizational design and reforms to clarify the office’s mission and responsibilities to better use its workforce and authorities to address emerging threats.

A Reform Agenda

TFI’s staff has, by any measure, performed exceptionally well under expanding demands. The reforms proposed here address three distinct but related deficiencies in TFI's current design. The first is a mission mismatch: TFI's name, internal structure, and component mandates still reflect a post-9/11 counterterrorism orientation that no longer describes the office's actual work. The second is an analytical gap: as the SEAD experience demonstrates, TFI lacks the permanent economic capacity its expanded mandate now requires. The third is an incomplete perimeter: Treasury's national security functions are scattered across offices with competing priorities, and the department has no criminal enforcement arm to complement its civil and regulatory tools. They are designed to be mutually reinforcing and new authorizing legislation, if required, would not span multiple congressional committees of jurisdiction.

New Name, Refined Mission: The Office of National Security and Financial Crimes

First, TFI should rebrand as the Office of National Security and Financial Crimes (NSFC). This name better captures the capabilities and mission of TFI, particularly when combined with other reforms recommended below. While “terrorism” as a framing made sense in the wake of the 9/11 terror attacks and the U.S. government’s subsequent response, terrorism is now just one of many priorities identified by TFI, competing over the past two decades with nation state threats spanning Iran, North Korea, Russia, and China as well as other transnational threats involving cybercrime and fraud, narcotics trafficking, and human rights/corruption. Similarly, “financial intelligence” is one (albeit highly important and valuable) tool used by TFI but the framing often confuses and intimidates, especially among private sector stakeholders as well as civil libertarians. We considered “Office of Economic Security,” but concluded that this framing is too expansive and does not capture the office’s financial crimes and criminal enforcement mandate. The name should describe the office’s functions, not the policy domain to which it contributes.

Consolidating the Core

Second, and more substantively, NSFC should administer a new merged bureau, the Office of Sanctions and Financial Crimes Enforcement (OSFCE); this reconstituted office would combine OFAC and FinCEN and incorporate TFFC’s policy function.

Over two decades, the missions of TFI have become more integrated, which should be viewed as a sign of success. However, stakeholders—ranging from intergovernmental colleagues to foreign officials to industry representatives and adversaries alike—do not meaningfully distinguish these functions. Many stakeholders conflate the various functions and bureaucratic representatives of financial sanctions (an OFAC authority), Section 311 special measures (a FinCEN authority), and Bank Secrecy Act compliance and enforcement (a FinCEN authority). An Under Secretary can and does coordinate these functions today, but coordination that depends on continual top-level attention is fragile; consolidating sanctions and AML/CFT enforcement under unified leadership makes integration the structural default rather than a recurring management burden.

Suboffices within OSFCE would still delineate between sanctions and AML/CFT functions. However, unified leadership and reporting would create efficiencies across all lines of bureaucratic business from consolidated and coordinated rulemaking, licensing, policy development, enforcement, and intra-agency, interagency, international and private sector engagement. Enforcement in particular could benefit from greater flexibility to deploy FinCEN and OFAC officers based on evolving needs under a common enforcement bureaucracy (and in coordination with the law enforcement reform below). This effort can build upon Alex Zerden and David Mortlocks’s 2024 recommendations in the Atlantic Council to increase enforcement resources and qualifications across FinCEN and OFAC. Congress has already identified the harmonization between FinCEN and OFAC, for instance by routing sanctions whistleblowers to FinCEN. The offices themselves already engage in joint April 2026 rulemaking for the GENIUS Act and parallel enforcement actions since 2022. This new structure would reflect the existing legal frameworks administered by FinCEN and OFAC. Where necessary, these reforms could involve legislative and regulatory changes. This proposal unquestionably requires significant consultation, further research, and planning to effect.

The merger will also address the redundancies and turf battles involving three policy offices and two intelligence functions. OIA would remain a standalone office given its separate legal authorities as part of the intelligence community; Atlantic Council experts have provided other helpful recommendations on OIA reforms separately. Such a proposal would not impact the United States’ compliance with the Financial Action Task Force (FATF). FinCEN is required to maintain an “operationally independent” financial intelligence unit to comply with FATF standards under Recommendation 29 and its Interpretive Note. Given the flexibility of financial intelligence unit design as allowed by FATF—and other models such as the United Kingdom’s embedding of its financial intelligence unit inside of its National Crime Agency—reorganizing FinCEN can be achieved while remaining compliant with FATF obligations.

Through this reorganization, the legacy OFAC function should include a standalone office of delisting —or, alternatively, a delisting function within its existing targeting, licensing, or compliance function—to further incentivize the dynamic and strategic use of sanctions, including through their responsible withdrawal on a more regularized basis. This idea appears to be gaining policy traction since we initially drafted this paper. On April 29, 2026, former DNSA and inaugural TFFC Assistant Secretary Juan Zarate floated the concept of strategic delisting during a public interview. On May 19, 2026, Treasury Secretary Scott Bessent provided updated guidance on sanctions use in a speech before the No Money for Terror conference where he outlined parameters to “adjust[]” sanction where necessary and avoid “linger[ing].” On May 26, 2026, the Treasury Department delisted 76 sanctions targets as part of a sanctions modernization initiative. Lastly, at a practical level, shrinking the number of NSFC offices allows for the integration of other elements into NSFC.

At a budgetary level, the NSFC’s budget must be coded by the Office of Management and Budget (OMB) as 050 alongside other national defense and security activities to solidify its national security mandate. The reform’s success will depend not only on the level of resources the NSFC receives but on their consistency and predictability; an analytical and enforcement capability built for sustained great power competition cannot operate on funding that fluctuates with each appropriations cycle. Such a move does not necessarily remove jurisdiction from the Treasury Department’s current appropriators, but it would protect NSFC from the budget battles that result in shutdowns of the Treasury Department when the national security enterprise typically resolves disputes more quickly. A more far-reaching option would fund NSFC through the NDAA; Treasury Department appropriators may demur but the urgency of reform and maintaining this national security capability warrants serious consideration.

Upgrading Analytical Capacity: A Chief Economist for National Security

The SEAD case study points to a staffing and design solution as much as an organizational one. NSFC should establish a permanent Chief Economist position at the Assistant Secretary level, reporting directly to the Under Secretary, with responsibility for economic and other analysis across all NSFC components-not just sanctions enforcement. This is the fix that SEAD's original design never achieved: analytical capacity with genuine institutional standing, a dedicated budget, and a reporting line that sits above any single component's equities.

The model already exists. The Justice Department's Expert Analysis Group — a group of approximately 50 Ph.D. economists embedded in the Department of Justice’s Antitrust Division — is led by the Deputy Assistant Attorney General for Economics, typically a prominent economist on leave from an academic post. That structure gives the economics function real authority within an enforcement-oriented department: its own identity, its own hiring pipeline, and a leadership position senior enough to push back on operational pressures. The result is analysis that informs enforcement decisions rather than getting absorbed by them. This is deliberately an economics-led function, not a multidisciplinary one. The intelligence, legal, and policy perspectives that national security decisions require are already well represented across TFI’s components—OIA, the offices of chief counsel, and TFFC. What has recurred as a binding constraint is the absence of permanent, senior economic capacity. A Chief Economist closes that specific gap; it does not displace the other lenses that already inform Treasury’s decisions.

An NSFC Chief Economist would do the same for economic statecraft. Rather than detailees rotating on six-month cycles through an OFAC org chart, the office would maintain a permanent professional staff of macro and financial economists capable of supporting sanctions design, AML/CFT policy, investment screening, and the kind of great-power economic scenario analysis that Muzinich and Singh correctly identified as missing from the U.S. government's toolkit. Housed at the NSFC level rather than inside any single component, the office would serve the full enterprise.

Completing the Perimeter

With the core consolidated and analytical capacity established, the final set of reforms expands NSFC’s perimeter to match the full scope of Treasury’s national security mission. Three additions complete the mandate: integrating investment screening functions currently housed outside TFI, restoring criminal enforcement capabilities, and establishing a civil liberties safeguard commensurate with NSFC’s expanded authorities. Outstanding questions raised in The Ledger about the role of the State Department in economic sanctions, including its targeting functionality, deserve further attention but fall outside of this Treasury-focused analysis.

Integrating Investment Screening

With fewer legacy offices in NSFC, room exists to expand NSFC’s mandate on both national security and financial crimes portfolios. On national security, the Treasury Department should migrate other national security functions from IA to NSFC—specifically, the Office of Investment Security, which chairs CFIUS, and the Outbound Investment Security Program. Currently, the Treasury Department expends resources deconflicting these functions between TFI and IA. This consolidation would bring the Treasury Department’s growing national security mission into one bureaucratic home while allowing IA to focus on its broader international economic mandate: exchange rate and currency policy, G7 and G20 macroeconomic coordination, bilateral economic diplomacy, sovereign debt, and U.S. representation at the international financial institutions.

Restoring Criminal Enforcement Capabilities with U.S. Secret Service

A reorganized NSFC should also have criminal as well as civil enforcement capabilities. The absence of a law enforcement arm within the Treasury Department’s Departmental Offices is itself a post-9/11 development: as Juan Zarate documented in Treasury’s War, much of TFI’s early success in developing novel civil and financial tools reflected a pivot away from criminal legal authorities that had previously anchored Treasury’s national security and law enforcement work. That pivot produced innovative policy tools, but left a gap. Civil sanctions and regulatory enforcement can freeze assets and impose compliance costs but cannot indict, arrest, or seize. For financial crimes with a clear criminal nexus—cybercrime, cryptocurrency fraud, sanctions evasion through shell company networks—the absence of in-house criminal investigative capacity forces reliance on the Department of Justice (DOJ), Federal Bureau of Investigation, and other law enforcement referrals that diffuse accountability. This occurs even in an environment of strong enforcement cooperation with the DOJ on deconfliction and parallel investigations.

Returning the U.S. Secret Service (USSS) to the Treasury Department is the most logical path to closing that gap. Though this proposal did not advance during the first Trump Administration, it was reintroduced in 2023, and the case has since grown stronger. USSS’s financial crimes mandate predates its protective mission and includes cybercrime, cryptocurrency investigation, and currency fraud—which already overlaps substantially with the Treasury Department’s enforcement priorities. Reuniting the two institutions would restore an operational pairing that existed for over a century before the post-9/11 reorganization moved USSS to DHS.

Given USSS’s increased weighting towards its protective mission, an alternative proposal could integrate and substantially modify the Treasury Department’s existing law enforcement agency, the Internal Revenue Service - Criminal Investigations (IRS-CI), into NSFC. Such a proposal would expand upon existing intra-agency coordination, such as the 2023 Binance cryptocurrency exchange enforcement actions by FinCEN, OFAC, and IRS-CI, as well as FinCEN/IRS-CI fentanyl trafficking targeting, and other shared priorities. Recognizing the political issues surrounding the IRS, additional modifications would be required to ensure the IRS-CI’s technical expertise benefits NSFC while materially reorienting the entity from its IRS origins.

Enhance Financial Privacy and Civil Liberties

Lastly, given these expanded capabilities, the NSFC’s last bureaucratic addition should be an administratively independent and adequately resourced ombudsman office for privacy and civil liberties that works across all NSFC components and programs to ensure the protection of constitutional rights. Unfortunately over much of the past decade, TFI and especially FinCEN and Bank Secrecy Act-derived information, has been subject to sustained politicization, leaks, and critiques. This empowered office will restore and maintain confidence in the sensitive data as well as the policies, procedures, and personnel who administer its lawful use.

Conclusion

The case for reform is not in dispute. The disagreement is about remedy.

Creating a Department of Economic Security is an appealing answer to a real problem. It is also the wrong one in the near term. The statutory complexity, operational costs, congressional gridlock, and ever-present risk of dismantlement by a successor administration are not hypothetical concerns—they are predictable consequences of attempting transformational reorganization in an environment that punishes institutional ambition.

There is also a substantive, not merely practical case against creating a DES. Sanctions and other financial measures derive their force from the same financial system Treasury is statutorily charged with protecting. Vesting both responsibilities in a single Cabinet officer—as the current structure does—allows those competing equities to be weighed inside one department rather than litigated between a new agency and a Treasury Secretary. Splitting them apart would create more friction than it resolves.

Defining the office’s remit also means being explicit about its limits. A reformed NSFC would do a specific set of things well: assess the economic and financial consequences of sanctions and other coercive measures before and after they are imposed; integrate financial intelligence, enforcement, and economic analysis under unified leadership; and serve as Treasury’s institutional home for the financial dimensions of national security. It would not—and should not—attempt to run industrial policy, manage supply-chain resilience, coordinate export controls, or arbitrate technology competition. Those functions belong to other departments with the requisite authorities and expertise; an office that tried to absorb them would reproduce the very overreach this paper warns against in the DES proposals. The value of the NSFC lies precisely in doing a bounded set of financial-statecraft functions with depth and durability, not in becoming a miniature Department of Economic Security inside Treasury.

The proposals outlined here work with the grain of existing institutions rather than against them. Much more work will be required to implement these recommendations; this paper provides a starting point to frame the efforts. Several key reforms – the TFI rebrand, the OFAC/FinCEN/TFFC consolidation, the Chief Economist, investment security functionality and ombudsman - require legislation within narrow committees of jurisdiction; others, like returning the Secret Service to Treasury, are medium-term objectives requiring broader Congressional action, but none require a decade to implement. The United States does not need a new department. It needs its existing economic statecraft apparatus to work—better resourced, better organized, and better calibrated to a threat environment that has moved well beyond the post-9/11 world that shaped TFI's original design.

Alex Zerden is the founder of Capitol Peak Strategies, a geoeconomic risk-advisory firm, an adjunct senior fellow at the Center for a New American Security, and an adjunct professor at the Georgetown University School of Foreign Service and American University Washington College of Law. Previously, he worked in the Treasury Department, including in the Office of Terrorism and Financial Intelligence as well as a financial attaché; at the White House National Economic Council; and in Congress.

Rachel Lyngaas is a senior policy researcher at the RAND Corporation and a professor of policy analysis at the RAND School of Public Policy. Previously, she served as the first Chief Sanctions Economist at the U.S. Department of the Treasury, where she founded and led the Sanctions Economic Analysis Division (SEAD) within Treasury's Office of Terrorism and Financial Intelligence. She has also held positions at the International Monetary Fund, Treasury's Office of International Affairs, the U.S. Department of State, and the board of the African Development Bank.

Editorial Note: Alex is also a member of The Ledger’s editorial board but recused himself from this submission’s double-blind editorial process.